The Backdoor Roth IRA

How You Could Generate Tax-Free Wealth at Retirement - Even with a High Income.

I was talking to a reader of our post on Section 529 Tricks.

He said he wasn’t able to take advantage of Trick #2 of rolling over up to $35,000 of his Section 529 funds into his Roth IRA because he didn’t have the latter due to a high income.

I told him there was a way he could still be eligible for a Roth IRA, and wanted to write a short post about it in case others felt they were in the same situation.

Summary

The IRS sets income limits for direct contributions to Roth IRAs, which can exclude high earners.

The Backdoor Roth IRA is a two-step process that allows individuals to contribute to a Roth IRA, regardless of their income level.

Initially, you contribute to a traditional IRA, which does not have income limits for contributions.

Subsequently, you convert the money from your traditional IRA to a Roth IRA. The critical aspect here is that conversions are not restricted by income levels.

The Benefits of Roth IRAs

Tax-Free Growth and Withdrawals: Roth IRAs offer tax-free growth and tax-free withdrawals in retirement, making them highly attractive for long-term savings.

No Required Minimum Distributions (RMDs): Unlike traditional IRAs and 401(k)s, Roth IRAs do not require minimum distributions during the account owner's lifetime, offering more flexibility in retirement planning.

Contribution Limits: The Roth IRA contribution limit for 2024 is $7,000 for those under 50, and an additional $1,000 catch up contribution for those 50 and older.

Estate Planning Advantages: Roth IRAs can be passed on to heirs, potentially providing tax-free income.

We show that by saving as early as possible, you save an additional $1.6 million at retirement - tax-free !

Want more?

Learn how you could boost your Roth IRA with a Mega Backdoor Roth IRA that increases the amount you can contribute.

Estimate how much you could have in retirement using Pre-Tax Strategies that could reduce your taxes now and nab you millions at retirement.

Disclaimer:

This post is for informational purposes only and does not constitute financial or investment advice. It is not intended to recommend any specific investment or provide a basis for making investment decisions. As the author, I am not a financial advisor, and my opinions should not be taken as financial advice. Investments carry risks and can fluctuate in value; past performance is not indicative of future results. Readers should conduct their own research or consult with a professional financial advisor before making any investment decisions. By reading this post, you agree that neither the author nor any affiliated entities shall be liable for any losses, damages, or claims that may arise from actions taken based on the information provided.

Introduction

In the complex world of retirement planning, the Backdoor Roth IRA stands out as a beacon for high-income earners seeking to navigate the restrictions of traditional retirement savings methods. This strategy has gained traction as a viable means to sidestep income limits and contribute to a Roth IRA, offering tax-free growth and withdrawals in retirement. In this post, we'll dive deep into the Backdoor Roth IRA, demystifying its workings, benefits, and considerations to help you decide if it's the right strategy for your financial future.

What is a Backdoor Roth IRA?

At its core, the Backdoor Roth IRA is not a distinct type of retirement account but a strategy that allows individuals to contribute to a Roth IRA, regardless of their income level. The IRS sets income limits for direct contributions to Roth IRAs, which can exclude high earners. However, by utilizing a two-step process involving a traditional IRA, individuals can effectively bypass these limits.

The Two-Step Process:

Contribution to a Traditional IRA: Initially, you contribute to a traditional IRA, which does not have income limits for contributions, although there are limits for tax-deductible contributions based on income and access to employer-sponsored retirement plans.

Conversion to a Roth IRA: Subsequently, you convert the money from your traditional IRA to a Roth IRA. The critical aspect here is that conversions are not restricted by income levels.

The Benefits of a Backdoor Roth IRA

Tax-Free Growth and Withdrawals: Roth IRAs offer tax-free growth and tax-free withdrawals in retirement, making them highly attractive for long-term savings.

No Required Minimum Distributions (RMDs): Unlike traditional IRAs and 401(k)s, Roth IRAs do not require minimum distributions during the account owner's lifetime, offering more flexibility in retirement planning.

Contribution Limits: The Roth IRA contribution limit for 2024 is $7,000 for those under 50, and an additional $1,000 catch up contribution for those 50 and older.

Estate Planning Advantages: Roth IRAs can be passed on to heirs, potentially providing tax-free income.

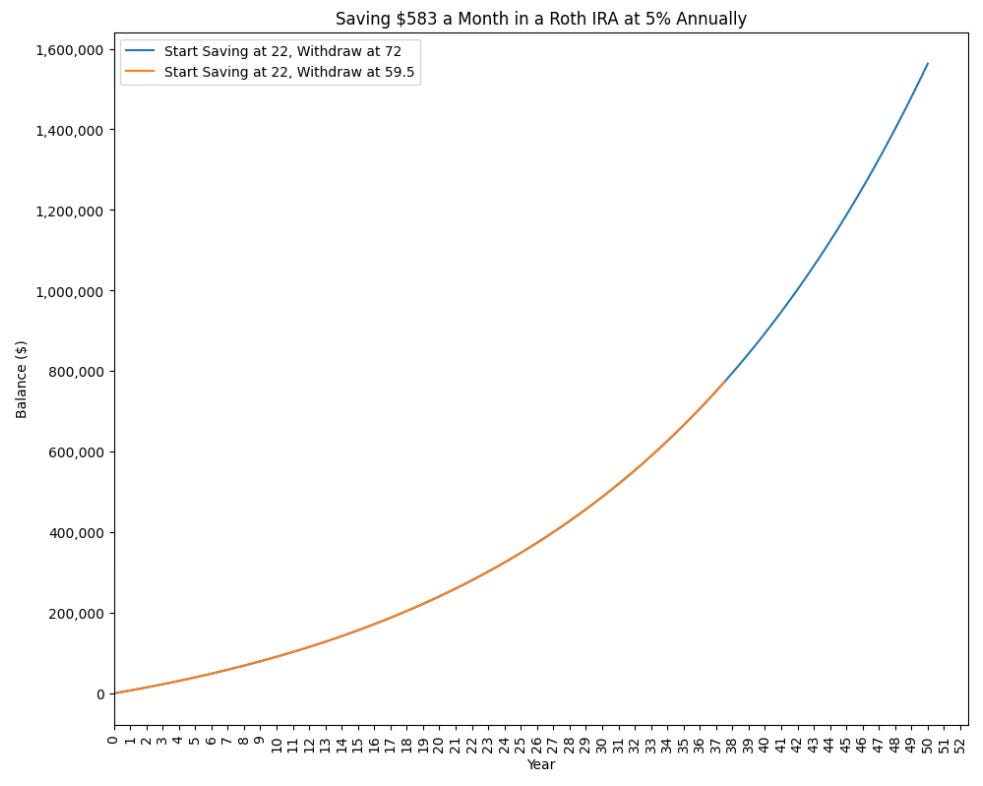

Start as Early as Possible.

You could have an additional $1.6 million to tap at retirement - tax-free!

To see this, let’s use our savings calculator with the below assumptions:

You max out your annual contributions each year. The limits usually increase year-over-year, but let’s assume it’s $7,000 a year for this simulation and you contribute $583.33 a month.

They grow at 5% annually, compounded monthly.

You do this from ages 22 - 59.5 (when the IRS allows withdrawals without penalty).

Below is how your savings could grow.

It could be up to $770,000 if you decided to withdraw at 59.5,

It could be up to $1.6 million if you decided to wait until 72.

This is great (tax-free !) income to live on or pass onto your beneficiaries in your estate.

Considerations and Cautions

Pro-Rata Rule: This rule can complicate the conversion process if you have existing pre-tax dollars in IRAs. It requires the calculation of taxes on the conversion based on the proportion of pre-tax and after-tax dollars across all your IRAs.

Tax Implications of the Conversion: The amount converted from a traditional IRA to a Roth IRA is taxed as ordinary income in the year of the conversion.

Timing: The timing of the conversion can significantly impact the tax implications, especially if your tax rate varies from year to year.

Sign-up for sessions at Quant Coaching today to learn more.

Is It Right for You?

The Backdoor Roth IRA strategy can be a powerful tool for retirement savings, but it's not suitable for everyone. Here are a few factors to consider:

Your Current and Future Tax Brackets: If you expect to be in a higher tax bracket in retirement, the tax-free withdrawals of a Roth IRA can be beneficial.

Your Estate Planning Goals: A Roth IRA's ability to provide tax-free income to heirs might align with your estate planning objectives.

Your Financial Situation: The immediate tax implications of the conversion and the potential complexity of managing pro-rata rules should align with your financial situation and goals.

Conclusion

The Backdoor Roth IRA offers a pathway for high earners to leverage the benefits of a Roth IRA. While it presents a unique opportunity for tax-free growth and withdrawals in retirement, it requires careful consideration and planning. Consulting with a financial advisor can provide personalized guidance to navigate the complexities of this strategy and ensure it aligns with your overall financial plan.

Remember, the journey to retirement is a marathon, not a sprint. Strategies like the Backdoor Roth IRA can be valuable tools in your arsenal, but they are most effective when part of a holistic approach to financial planning.

Sign-up for sessions at Quant Coaching today to learn more about investing.